What Happens If (When) USD Trends Higher?

Dollar Ain't Dead

Dollar sentiment has been as negative as imaginable over the past several months. Extraordinarily loose monetary policy has pointed toward a hole that continues to grow and the Fed can only throw so many dollars into that hole to soften the fall. The weight of dollar output from our fine-tuned printing presses is unbearable.

Washington surrendered their strong dollar talk more than one year ago. Nobody took it seriously anyway. Sure, a strong dollar sounds great, but it of course would only worsen an already shoddy trade deficit. You can’t have them both. The plan was to deflate USD to keep our goods looking attractive. Was that a success? Hard to say but but when a major trade competitor in the ags space let their currency deflate even more, that move was nullified. Grains from Brazil looked awfully attractive through the 1st half of 2020 as the Real tanked. If you don’t think the U.S. Dollar can rally, just look at the chart below where USDBRL ran up though the first 5 months of 2020.

So why now? Why would the greenback make a move higher? Washington remains firmly behind a weak dollar and continue to punt a rate hike down the road a few years.

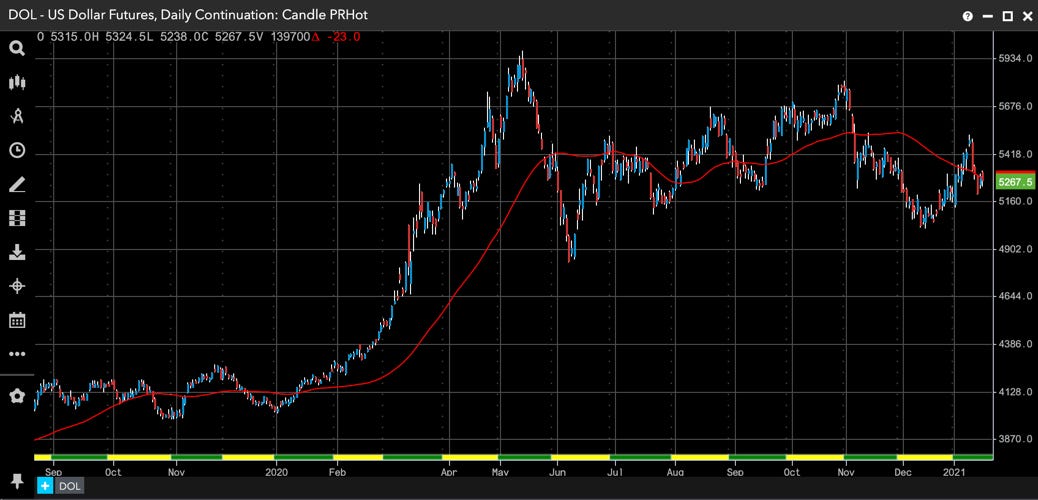

Markets are questioning the Fed’s resolve here. Look at Treasuries. 30-yr futures are trading down around their lowest level in 11 months. Goldman Sachs has moved in their date for a rate hike to the 2nd half of 2024. Grains, despite the fallout of BRL, are on fire. Copper, lumber and long list of commodity prices are elevated to pre-pandemic levels.

How do we manage to generate inflation during a pandemic? We’ve burned that wick from both ends.

Where’s supply? Shut-downs have certainly limited production. We simply don’t have the goods the meet demand. Tradewar antics are also affecting prices. China v. Australia pushed iron ore prices higher through the year. Mines in Brazil also ran into production problems related to Covid. The metals shortages provided fire to lift a great deal. When iron ore rise, steel has to rise. When steel rise, building and car prices rise. Speaking of cars, now the U.S. auto industry is suffering from a shortage of vital computer chips that come from China.

Demand? We still need goods. Regardless of the pandemic, we need stuff and when the government is cutting checks to just about everyone, they’re going to use it. Was it wise to give relief funds to those who jobs were not impacted by the pandemic? Hmmm. They generate demand. Too much demand, perhaps. Too much money chasing too few goods is economics 101 for inflation.

How much of this inflation can the Fed take before raising rates? That’s the million dollar question. It’s absolutely a leading story to watch this year. How long can the U.S. hold out before raising rates.

So back to The Dollar. Let’s say it does run higher. Wall Street has been pounding the table for a big year in commodities. It’s their time and ags, metals, softs and more should explode in 2021. We’re seeing that already. Will it last? If USD is indeed getting ready to trend higher, can commodities go with it? That’s not a likely scenario. One of them has to give.

I’d love to hear your thoughts. Convince me I’m wrong.